MINI PROJECT GROUP 3 - POH KONG

GROUP MEMBERS

1. SYAHIR ADAM BIN RAMLAN

10DAT21F2019

2.NUR ALIA MAISARAH BINTI NASIR

10DAT21F2023

3. PHAVINISHAA A/P VIKNESWARAN

10DAT21F1019

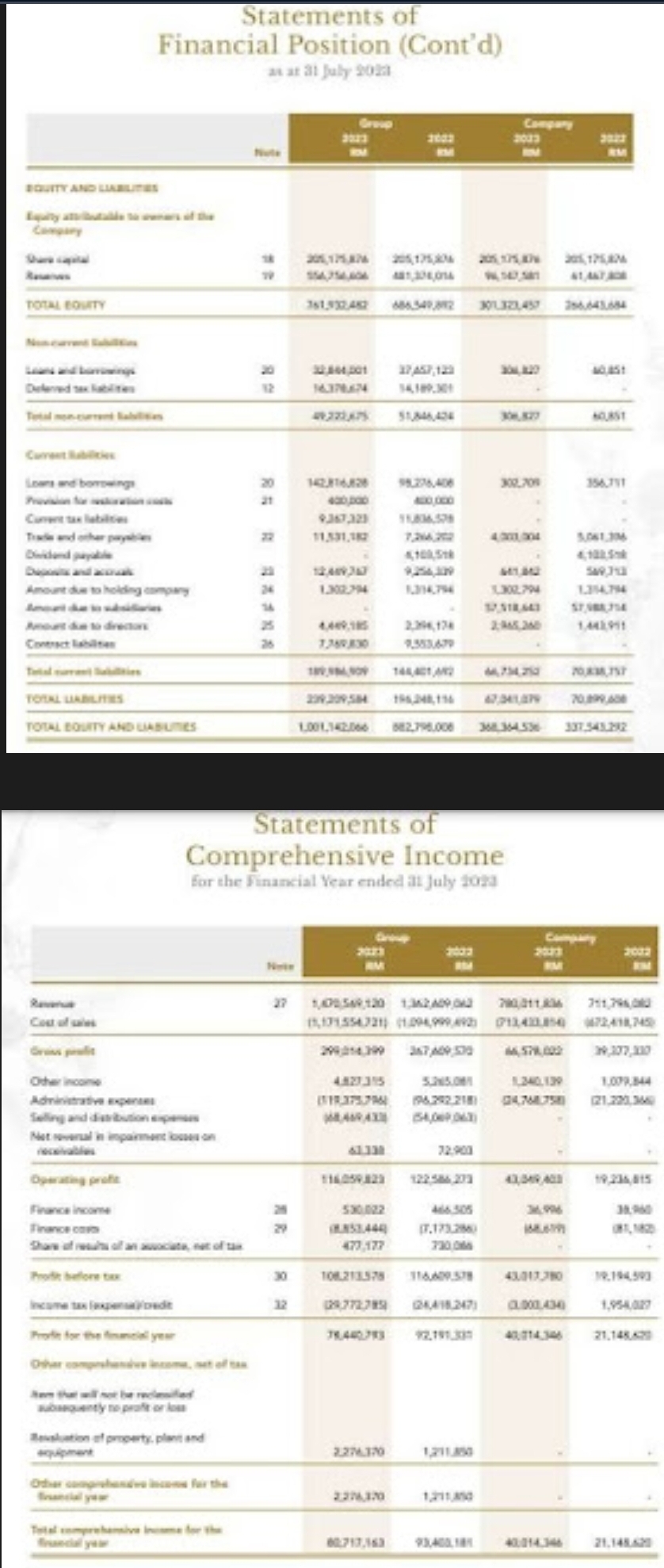

PART A - ANNUAL REPORT OF POH KONG

PART B

Part B : Analyzing Problems

Calculate the financial ratios for 2years (2022 and 2023) and provide an analysis of the significant ratio changes for 2 years. Please calculate the financial ratios in the table below:

PART C QUESTION 1

various effects on its business risk, status as a going concern, and relevant issue.

1. *Business danger*:

- *Lower Financial Risk*:

A reduction in debt lowers the financial leverage of the business, which in turn lowers the danger of default and financial hardship.

- *Improved Profitability*:

Better performance is indicative of increased profitability, which can strengthen an organization's resistance to market pressures and economic downturns.

2. *Going Concern Status*: -

*Stability and Sustainability*:

A more stable financial position improves the company's capacity to fulfill its commitments and continue operations over the long run. Higher profitability and reduced debt help achieve this.

- *Positive Cash Flow*:

The company's liquidity and capacity to finance ongoing operations and investments are supported by improved cash flow creation brought about by lower debt commitments and higher profitability.

3. *Relevant Issues*:

- *Investment Opportunities*:

The company may have more funds available for strategic investments, R&D, innovation, and market expansion as a result of higher profitability and lower debt.

- *Stakeholder Confidence*:

Strong financial results can encourage loyalty and trust among stakeholders, including customers, workers, shareholders, and others.

Generally, a company's enhanced financial health and resilience are indicated by higher profitability and lower debt, and this can have a favorable effect on the company's business risk, going concern status, and related difficulties. To guarantee long-term success, it is crucial to keep an eye on operational efficiency, market conditions, and other aspects.

Part C QUESTION 2

The following actions can be performed to confirm data derived from analytical procedures:

1. Examine the supporting documentation for management statements, including the annual reports, SOPs, and organizational policies.

2. Examine material from other sources that was used in the analysis, such as industry research, statistical data, and reports on market research.

3. Verify the information from the analysis's results is compatible with data from external sources and management documentation.

4. Verify the analytical techniques and methodology to make sure the outcomes are accurate and reliable.

5. Speak with stakeholders or industry experts to get further information or reassurance about the analysis that was done. 6. Use cross-checking to compare analysis findings with data or studies from various sources.

7. Perform a cross-audit to contrast the analysis's conclusions and findings with those of an audit carried out by a third party or expert.

8. Based on the suitability and consistency of the information gleaned with the facts or patterns discovered in credible sources, make an evaluation.

By providing additional audit proof to back up the information gleaned from analytical techniques, these steps will assist guarantee its accuracy and dependability.

Part C QUESTION 3

In order to comprehend the fundamental causes of the observed variances, the following extra audit methods can be recommended:

1. *Comparative Analysis*:

To find long-term patterns and changes that might have an impact on the variations, trends and variations are compared with those from prior years or with industry benchmarks.

2. *Interviews with Management and Staff*:

To get their opinions on the variables that could be causing the variation, senior management and employees participating in the pertinent process should be interviewed.

3. *Operational Process Inspection*: Examines work procedures and operational processes to find flaws or modifications that could impact performance and offer details to help explain such differences.

4. *Business Change Study*:

Examine any modifications to the company's strategy, adjustments to the market, or any outside variables that could have an impact on financial performance and business decisions.

5. *Compliance and Risk Analysis*:

Evaluate how well rules and processes are being followed, and pinpoint any risks that could have an impact on and lead to variations in financial performance.

These extra audit techniques will facilitate proper care in evaluating the impact and implementing the necessary actions, as well as aid in gaining a deeper understanding of the underlying causes behind the deviations discovered

Comments